Deeper understanding leads to better outcomes

Disclosures

4. SMBC Nikko Securities America, Inc.

Anti-Money Laundering

Summary of Anti-Money Laundering (AML) Related Information and Company Status with Regulators

SMBC Nikko is a registered broker-dealer with the SEC and a member of the self-regulatory organizations, FINRA and MSRB. As such, SMBC Nikko is considered a "covered financial institution" for purposes of the U.S. Bank Secrecy Act, as amended by the USA PATRIOT Act and is subject to the regulations thereunder, as well as the rules and oversight of the federal regulatory agencies and self-regulatory organizations listed above.

Our policy is to prohibit and actively prevent money laundering and any activity that facilitates money laundering or the funding of terrorist or criminal activities. Money laundering generally is defined as engaging in acts designed to conceal or disguise the true origins of criminally derived proceeds so that the unlawful proceeds appear to have been derived from legitimate origins or constitute legitimate assets.

Customer Identification Program

To help the government fight the funding of terrorism and money laundering activities, federal law requires us to obtain, verify and record information that identifies each person or entity who opens an account. When you open an account, we are required to ask for certain identifying information such as your legal name, address, and other information that will allow us to identify you. We also may ask to see identifying documents to verify your identity and to screen your name against various government databases.

Notice Regarding Entities Identified as Being of Primary Money Laundering Concern

Pursuant to U.S. regulations issued under section 311 of the USA PATRIOT Act, 31 CFR 103.192, we are prohibited from opening or maintaining a correspondent account for, or on behalf of, certain Specified Banks. The regulations also require us to notify you that your correspondent account (if applicable) with our financial institution may not be used to provide the Specified Banks with access to our financial institution. If we become aware that the Specified Banks are indirectly using the correspondent account (if applicable) you hold at our financial institution, we will be required to take appropriate steps to prevent such access, including terminating your account.

Business Continuity Plan

Sumitomo Mitsui Banking Corporation ("SMBC”) is committed to maintain a duty of care as to our staff, protect our and our customers’ assets and information, and minimize financial, legal/regulatory, and reputational impact in the event of an operational disruption, major internal or external incident, or crisis event.

In furtherance of this commitment, SMBC maintains a comprehensive Business Continuity Management Program (the “Program”) to provide appropriate resilience and recovery for critical business processes, systems, and data as needed.

The Program is derived from and adheres to a number of regulatory, governmental, and industry standards and guidelines, including, without limitation:

FINRA Rule 4370 (General BC Requirements);

NYSE IM 05-80 (General BC Requirements);

CFTC Rule 23.603 (Business Continuity and Disaster Recovery);

NFA Rule 2-38 (General BC Requirements);

FFIEC Exam Handbook (IT BC Requirements);

US Treasury 2008 Strategic Plan (Treasury Auction OOR Requirements);

FRB SR Letters (including 03-09 – Sound practices and 13-19 – Outsourced risk);

and related regulations, standards, and guidelines in Brazil, Canada, Latam, and the Cayman Islands.

The Program is regularly audited internally and externally and SMBC actively engages with industry groups regarding resiliency within the financial sector to stay abreast of any developments and ensure our Program is adequate.

The Program includes:

- Crisis management plans to manage critical functions during and following any significant business disruption;>

- Documented procedures to back-up and recover critical systems and data; and

- Communication plans for key stakeholders, including clients, employees, partners, and vendors.

SMBC has a dedicated team of business continuity professionals whose job is to ensure that Program is documented, reviewed, and tested in line with all applicable standards.

The Program is supported by the Board of Directors and governance committees

Should you have any specific questions about our Program, we encourage you to bring those to your SMBC Relationship Manager.

Securities Exchange Act Rules 606 and 607

Securities Exchange Act Rule 606 - Routing Statistics

SMBC Nikko publishes quarterly reports pursuant to SEC Rule 606(a) broken down by calendar month, containing certain required statistical information regarding the routing of held, non-directed customer orders in Regulation NMS stocks and listed options in NMS securities, including the nature of any relationship SMBC Nikko has with each venue. In addition, customers of the firm may request in writing details on NMS stock and option non-directed orders in NMS securities including the identity of the venue and the time of execution for the prior six months as required under Rule 606 (b)(1). SMBC Nikko is required to provide under certain circumstances additional routing and execution reports of the customer’s NMS stock orders submitted on a not held basis for the prior six months under Rule 606 (b)(3) within seven days of customer’s request.

SEC Rule 606(a) Reports from Q2 2024 to present can be accessed on the FINRA Public Portal

SEC Rule 606(a) Reports required prior to Q2 2024 can be accessed on the SMBC Nikko Public Portal

Securities Exchange Act Rule 607 - Disclosure of Payment for Order Flow

SMBC Nikko does not receive payment for order flow. In its efforts to provide for best execution, SMBC Nikko may route customers’ equity orders to one or more exchanges, alternative trading systems, electronic communications networks and other market centers. Certain of these execution venues offer cash credits/rebates or charge fees for orders depending on whether the orders provide liquidity to or take liquidity from the market. Periodically, the amount of credits/rebates that SMBC Nikko receives from one or more such execution venues may exceed the amount that the Firm is charged.

FINRA RULE 2266 – SIPC Information

Pursuant to FINRA Rule 2266, we are required to notify you of the following:

- Customers may obtain information about insurance provided by the Securities Investor Protection Corporation or SIPC, including the SIPC brochure, by contacting SIPC

- SIPC’s web site address http://www.sipc.org/ and telephone number (202) 371-8300

FINRA RULE 2267 – Investor Education and Protection

FINRA runs a public disclosure program known as BrokerCheck that provides information about brokerage firms and their registered persons. To obtain an investor brochure that includes information about BrokerCheck or to obtain additional information, contact the FINRA public disclosure hotline at (800) 289-9999 or visit the BrokerCheck website at http://brokercheck.finra.org/. FINRA’s general website is located at http://www.finra.org/.

FINRA RULE 5270 - Prohibition on Front-Running of Block Transactions

SMBC Nikko is generally prohibited from trading for its own account while in possession of an imminent (non-public) customer block order transaction (material market information), or providing such information to other investors or market participants, prior to the time the block transaction has been made publicly available (e.g. - reported executed) or, due to the passage of time, the order information has become stale or obsolete. Rule 5270 does not preclude principal transactions that SMBC Nikko can demonstrate are unrelated to the block order information. These may include transactions:

- where the Firm has established information barriers designed to prevent disclosure of such information;

- to correct bona fide errors;

- to offset odd-lot orders; or

- to purchase or sell individual or related securities or derivatives to unwind a facilitation position, or to hedge / pre-hedge the Firm’s risk in preparing for and executing block orders.

To manage its risk, SMBC Nikko may trade as principal at the same time and at the same price level in fulfilling your block order. SMBC Nikko may also trade along with your block order in the underlying security or related securities (derivatives) to the extent that its principal trading activity hedges or mitigates risk. In such cases, SMBC Nikko will seek fair and equitable allocations of order fills between your account and its principal account.

Trading in Securities Subject to a Distribution (SEC Regulation M, Rule 105)

SEC Rule 105 of Regulation M generally prohibits any person that sold short securities subject to a public securities offering within a specified period of time immediately preceding the pricing of the offering from purchasing the securities in that offering. For additional information on Rule 105, please see the SEC’s adopting release, available at:http://www.sec.gov/rules/final/2007/34-56206.pdf. We rely on your obligation to understand and comply with the provisions of Rule 105 as it pertains to your trading activity when you seek or accept an allocation in a public securities offering from SMBC Nikko.

FINRA RULE 5310 – Best Execution

In any transaction for or with a customer, SMBC Nikko will use reasonable care in seeking to obtain the most advantageous terms reasonably available under the circumstances for the execution of a customer’s order. In determining where to send customers’ orders SMBC Nikko takes into consideration, among other things, the size and type of order, the terms and instructions of the order, the trading characteristics of the security, the character of the market for the security, the accessibility of quotations, transaction costs, the opportunity for price or size improvement, the speed of execution, the availability of efficient and reliable order handling systems, the level of service provided by the market venue and the customer’s overall objectives with respect to the market conditions at the time of the order. SMBC Nikko regularly reviews transactions for quality of execution.

FINRA RULE 5320 - Trade Along, Not Held Orders

Customer equity orders received by SMBC Nikko are deemed “Not Held” orders unless you (customer) specifically request and provide other specific order instructions. A “not held” order means you are giving SMBC Nikko time and price discretion in seeking to obtain the best execution of your order.

When handling “not held” limit orders for institutional customers, SMBC Nikko is not required to display or protect the limit order. SMBC Nikko may trade for its own account at prices equal to, or better than, those of “not held” orders and orders of 10,000 shares or more unless the institutional customer opts into Rule 5320 protection from SMBC Nikko trading at prices equal to or better than those of the institutional customer’s order. Clients may “opt in” to the Rule 5320 protections by providing written notice to their SMBC Nikko sales representative. Notwithstanding the foregoing, SMBC Nikko makes every reasonable effort to provide you with the best execution possible.

Handling orders on a Not Held basis also means that SMBC Nikko may on occasion simultaneously conduct same-side principal trading in the same or related products while your order is outstanding. Principal trading while in possession of a customer order is allowed and may occur with knowledge of the customer order, as pre-positioning and anticipatory hedging for the overall benefit of the customer order.

Guaranteed Benchmark Orders

We may receive orders from you and/or other clients for equity securities where we agree to execute in a principal capacity all or a portion of the order at a guaranteed price. That price may be based on a benchmark such as VWAP or the official closing price for the security. We make every reasonable effort to facilitate your guaranteed price orders but may not, under certain circumstances, execute such orders fully or at all (e.g., a primary exchange fails to publish a closing price, the inclusion of the security on our restricted list, a trading halt (regulatory or otherwise), or another regulatory restriction.) In order to minimize or offset the risk of such guaranteed price transactions, we may engage in hedging or other positioning activity prior to executing your order, including but not limited to buying or selling the security(ies) that is/are the subject of the order or buying or selling an option or a future on the underlying security or basket of securities. While it is possible that such risk mitigating activities or other client activities could impact the benchmark price or the market for the security(ies) that is/are the subject of the order and, consequently, your costs or proceeds on the transaction, we will make every reasonable effort to minimize such impact. Any profit or loss from our risk mitigating activities will accrue to SMBC Nikko.

Regulation SHO Fail-to-Deliver Buy-In Requirement

Customers are advised to make every effort to settle their transactions timely.

In the event that you sell equity securities “short” through SMBC Nikko and the securities are not delivered to SMBC Nikko by the settlement date (T+1), borrowed securities must be received or the short position must be bought-in by no later than the opening of trading on the morning after settlement date (T+2). Customers who fail to timely deliver securities sold short will be required to pay for purchased securities. Customers who are unable to resolve failed delivery of securities to satisfy a short sale position may be prohibited from effecting further short sales in the security.

In the event that you sell equity securities ("long") through SMBC Nikko and the securities are not delivered to SMBC Nikko by the settlement date (T+1), delivery must be made no later than before the opening of trading on T+5.

SMBC Nikko may impose other conditions or limitations on trading should the client exhibit a pattern of fails.

Trading Indications of Interest and Trade Advertising

As used in this context, an IOI is an expression of trading interest that contains one or more (but not all) of the following trade elements: security name, size, side, capacity, and price. The use of an IOI is intended to solicit contra-side interest. We may submit an IOI to another market participant or trading venue. IOIs may be disseminated over electronic trading systems or through direct connections to clients' order management systems. When submitting IOIs, we will adhere to service providers' guidelines and guidance issued by regulators, including whether we designate an IOI as “natural”, (a client order or principal order effected to facilitate a customer order). We use certain service providers (e.g., Bloomberg) to advertise trade executions. Customers may opt out of advertising their executions and/or submitting IOIs by contacting your SMBC Nikko sales representative.

Large Trader Identification - SEC Rule 13h-1

SEC Rule 13h-1 defines certain investors ("Large Traders") that in the aggregate effect transactions in NMS securities that are equal to or greater than:

- During a calendar day, either two million shares or shares with a fair market value of $20 million; or

- During a calendar month, either twenty million shares or shares with a fair market value of $200 million.

Customers who are registered as Large Traders are required to notify SMBC Nikko and provide their Large Trader Identification Number (“LTID”). SMBC Nikko monitors its customers for compliance with SEC Rule 13h-1’s large trader registration requirement. SMBC Nikko keeps records of the activity of all of its customers and is obligated to report large trader transaction information to the SEC upon request. If a customer has not provided an LTID and its trading activity triggers the large trader thresholds, SMBC Nikko will notify the customer of its obligations and self-identification requirements under Rule 13h-1.

Rule 15c3-5 and Market Access

SEC Rule 15c3-5 requires broker-dealers that access or provide access to exchanges or alternative trading systems to establish, document and maintain a system of risk management controls that are reasonably designed to manage the financial, regulatory and other risks in connection with market access. SMBC Nikko has in place controls that will reject orders that exceed pre-determined risk parameters.

U.S. Treasury Securities Fails Charge

SMBC Nikko follows the U.S. Treasury Securities Fails Charge Practice published by the Treasury Market Practices Group (“TMPG”) and the Securities Industry Financial Markets Association (“SIFMA”). Accordingly, any failure by you to deliver Treasury Securities by settlement date in transactions we have with you is subject to a Fails Charge as published by TMPG and SIFMA. See: TMPG | Treasury Market Practices Group (newyorkfed.org)

U.S. Treasury Securities Information Handling

SMBC Nikko follows the U.S. Treasury Securities Information Handling Practices published by the Treasury Market Practices Group (“TMPG”). Accordingly, SMBC Nikko America maintains policies, procedures, and a training program on covering the handling, sharing and use of confidential information and material non-public information (“MNPI” or “inside information”), and the maintenance and safeguarding of client confidentiality. SMBC Nikko America applies a “need to know” standard with respect to all aspects of client information including but not limited to order, quotation, execution, positional, and pricing data, and such information may be used by staff only for its intended purposes. See: TMPG | Treasury Market Practices Group (newyorkfed.org)

SMBC Nikko Securities America, Inc. Notice Regarding Japanese Government Bond (“JGB”) Transactions Referencing the BB Prices (Closing Prices) Published by Japan Bond Trading Co., Ltd.

SMBC Nikko Securities America, Inc. (“Nikko America”) may conduct proprietary hedging, pre-hedging and/or pre-positioning transactions after receiving an indication of interest from a customer to engage in a transaction in JGBs based on Closing Prices (defined below), before the transaction between the customer and Nikko America is finalized based on such Closing Prices. In connection with JGB transactions, the term “Closing Prices” means those Bloomberg closing prices in JGBs published by Japan Bond Trading Co., Ltd.

These hedging transactions are conducted in accordance with Nikko America’s internal policies and procedures, and applicable laws and regulations, with the goals of mitigating the risks borne by Nikko America as well as minimizing market impact. They are also intended to enable Nikko America to offer fair and competitive trading terms to customers, including liquidity provision and spreads relative to the Closing Prices. Please note, such hedging activities may potentially influence market prices and liquidity in JGBs. Nikko America does not engage in hedging transactions with the intention of disadvantaging customers or disrupting the market, and Nikko America may transact with or utilize one or more of its affiliates, such as SMBC Nikko Securities, Inc. (“Nikko Tokyo”), to facilitate such Closing Price transactions.

If a customer explicitly requests that Nikko America refrain from conducting hedging transactions prior to the determination of the Closing Prices, Nikko America may use discretion as to whether it can comply with such request. However, in such cases, if Nikko America cannot accommodate the client request, the firm may decline to execute the relevant JGB transaction.

Please note that Nikko America’s affiliate Nikko Tokyo, has a capital relationship with the Japan Bond Trading Co., Ltd.

FINRA Rule 2265 - Extended Hours Trading Risk Disclosure

While extended hours trading can provide customers with greater opportunities to trade securities and manage their portfolios, it also involves material risks that are specific to extended hours trading.

Extended Hours Trading Risk Disclosure Statement

- You should consider the following points before engaging in extended hours trading. "Extended hours trading" means trading outside of "regular trading hours." "Regular trading hours" generally means the time between 9:30 a.m. and 4:00 p.m. Eastern Standard Time.

- Risk of Lower Liquidity. Liquidity refers to the ability of market participants to buy and sell securities. Generally, the more orders that are available in a market, the greater the liquidity. Liquidity is important because with greater liquidity it is easier for investors to buy or sell securities, and as a result, investors are more likely to pay or receive a competitive price for securities purchased or sold. There may be lower liquidity in extended hours trading as compared to regular trading hours. As a result, your order may only be partially executed, or not at all.

- Risk of Higher Volatility. Volatility refers to the changes in price that securities undergo when trading. Generally, the higher the volatility of a security, the greater its price swings. There may be greater volatility in extended hours trading than in regular trading hours. As a result, your order may only be partially executed, or not at all, or you may receive an inferior price when engaging in extended hours trading than you would during regular trading hours.

- Risk of Changing Prices. The prices of securities traded in extended hours trading may not reflect the prices either at the end of regular trading hours, or upon the opening the next morning. As a result, you may receive an inferior price when engaging in extended hours trading than you would during regular trading hours.

- Risk of Unlinked Markets. Depending on the extended hours trading system or the time of day, the prices displayed on a particular extended hours trading system may not reflect the prices in other concurrently operating extended hours trading systems dealing in the same securities. Accordingly, you may receive an inferior price in one extended hours trading system than you would in another extended hours trading system.

- Risk of News Announcements. Normally, issuers make news announcements that may affect the price of their securities after regular trading hours. Similarly, important financial information is frequently announced outside of regular trading hours. In extended hours trading, these announcements may occur during trading, and if combined with lower liquidity and higher volatility, may cause an exaggerated and unsustainable effect on the price of a security.

- Risk of Wider Spreads. The spread refers to the difference in price between what you can buy a security for and what you can sell it for. Lower liquidity and higher volatility in extended hours trading may result in wider than normal spreads for a particular security.

MSRB Rule G-10 – Investor Education and Protection

SMBC Nikko is subject to the regulations and rules on municipal securities activities established by the SEC and MSRB. The website for the SEC is www.sec.gov and the website for the MSRB is www.msrb.org. Note that in addition to having educational material about the municipal securities market, the MSRB website has an investor brochure that describes the protections that may be provided by the MSRB rules and how to file a complaint against SMBC Nikko or a SMBC Nikko representative with the FINRA Investor Complaint Center. To obtain a copy of MSRB Rules, contact the MSRB at (202)-838-1500 or visit MSRB website.

Municipal Entities and Obligated Persons Disclaimer

If you are a municipal entity or obligated person, (a) SMBC Nikko is not recommending to you any action; (b) SMBC Nikko is not acting as an advisor to you and does not owe a fiduciary duty pursuant to Section 15B of the Securities Exchange Act to you with respect to the information and material contained in this communication; (c) SMBC Nikko is acting for its own interests; and (d) you should discuss any information and material contained in this communication with any and all internal or external advisors and experts that you deem appropriate before acting on this information or material.

Telephone Recording Disclosure

SMBC Nikko records certain phone lines of our sales and trading personnel. Please note that these recordings may be made without the use of a spoken warning, tone, or similar notification. Please be advised that participation in such calls by your employees or representatives constitutes consent to such recording where consent is required under applicable law.

Privacy Disclosure

SMBC Nikko Securities America, Inc. aligns its information privacy policy with the SMBC Americas Division policy. See the disclosures at https://www.smbcgroup.com/americas/privacy-security.

Disclosure to Canadian Clients Under National Instrument 31-103

As a client of SMBC Nikko, resident in a jurisdiction of Canada, you are advised that we operate as a dealer or adviser in your jurisdiction under an exemption from the dealer and adviser registration requirements contained in National Instrument 31- 103 - Registration Requirements and Exemptions (NI 31-103) and, as such, we are not required to be and are not a registered dealer or adviser in your jurisdiction.

As required, in order to operate under the international dealer and international adviser exemptions, we wish to notify you of the following:

- Our head office is located at 277 Park Avenue, Fifth Floor, New York, New York, 10172; and

- You may face difficulty in enforcing legal rights you may have against us because we are resident outside of Canada and all or substantially all of our assets are situated outside of Canada.

Purchaser Representations

As a condition of providing our services to you, you are deemed to represent to us that you are, (i) purchasing as principal; (ii) an accredited investor, as defined in National Instrument 45-106 Prospectus Exemptions or subsection 73.3(1) of the Securities Act (Ontario), and (iii) a permitted client, as defined in NI 31-103. Any resale of the securities you acquire in an offering must be made in accordance with an exemption from, or in a transaction not subject to, the prospectus requirements of applicable securities laws.

Statutory Rights

Securities legislation in certain provinces or territories of Canada may provide you with remedies for rescission or damages if the offering document used in connection with an offering (including any amendment thereto) contains a misrepresentation, provided that the remedies for rescission or damages are exercised by you within the time limit prescribed by the securities legislation of your province or territory. You should refer to any applicable provisions of the securities legislation of your province or territory for particulars of these rights or consult with a legal advisor.

Underwriting Conflicts

Pursuant to section 3A.3 (or, in the case of securities issued or guaranteed by the government of a non-Canadian jurisdiction, section 3A.4) of National Instrument 33-105 Underwriting Conflicts (NI 33- 105), we are not required to comply with the disclosure requirements of NI 33-105 regarding underwriter conflicts of interest in connection with an offering.

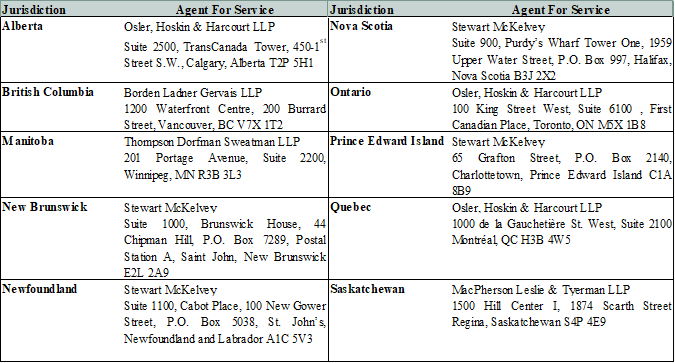

Agent for Service

We have appointed Agents for Service in Canada as indicated in the table below:

Disclosure to Australian Clients Under Class Order 03/1100

SMBC Nikko Securities America, Inc. (“Nikko America”), which is exempt from the requirement to hold an Australian financial services license under Australia’s Corporations Act 2001 (Cth) in respect of the financial services being provided to you. Nikko America is authorized and regulated by the U.S. Securities and Exchange Commission under the laws of the Exchange Act of 1934, as amended, which differ from Australian laws and is a member of the Financial Industry Regulatory Authority, which is a U.S. self-regulatory organization with its own rules and regulations. This document is distributed only to wholesale clients as that term is defined under Australia’s Corporation Act 2001 (Cth). This document is not intended for distribution or dissemination, directly or indirectly, to any other class of persons. It is being supplied to you solely for your information and may not be reproduced, forwarded to any other person or published, in whole or in part, for any purpose.

Statement of Financial Condition

Copies of SMBC Nikko’s audited and unaudited financial statements are available for you to review, print, and download:

- Unaudited Statement of Financial Condition 6/30/2026

- Audited Statement of Financial Condition 12/31/2025

Transparancy & Reporting

Pursuant to the Financial Instruments and Exchange Law of Japan, effective as of March 1, 2016, a person who has submitted a notification regarding Specially Permitted Businesses for Qualified Institutional Investors, etc. is required to make available to the public certain information. Information on the following entities can be obtained upon request:

If you would like to obtain information, please send an email to WaterLily@smbcgroup.com.

Contact Information for SMBC Nikko Securities America, Inc.

For more information or questions, please contact us at NKCompliance@smbcnikko-si.com.

Contact for Customer Complaints

To file a complaint, please contact us at NYNikkoComplaintsExternal@smbcnikko-si.com.

6. SMBC SOFOM, S.A.P.I. DE C.V., SOFOM, E.N.R.

English Version

About us

Multiple Purpose Financial Companies (SOFOM) are a type of company in Mexico, whose main purpose is to carry out one or more of the activities of granting credit, leasing or financial factoring; these types of companies must have a current registration with the National Commission for the Protection and Defense of Users of Financial Services (Comisión Nacional para la Protección y Defensa de los Usuarios de Servicios Financieros, CONDUSEF).

This type of companies operate similarly to a bank, save and except that they are not allowed to raise funds from the general public and are not heavily supervised by the Mexican authorities.

In March 2015, SMBC SOFOM officially started its operations with only one authorized product - Term Loans (Single Draw).

SMBC SOFOM currently offers the following services:

- One-time and deferred drawable term loans (subject to liquidity coverage by means of capital)

- Revolving Credit / GTFD (subject to liquidity coverage using capital)

- Project Financing - Utilizing the Banobras (Development Bank) financing facility (long-term financing in MXN)

- Financial leasing (MXN or USD)

- Derivatives

Specialized User Service Unit:

The purpose of the Specialized User Service Unit (UNE) of SMBC SOFOM is to attend to the Inquiries, Complaints and Clarifications of the Users of the services provided by it and shall provide the National Commission for the Protection and Defense of the Users of Financial Services (CONDUSEF) with the information related to the UNE and the way to identify or locate its owner.

In this regard, SMBC SOFOM shall receive the referred Inquiries, Claims and Clarifications from its clients, through the Reception Means it designates for such purposes, acknowledge receipt to the clients, assign a folio number and indicate the response or resolution time. Likewise, the corresponding resolution or response must be communicated to the client by the means indicated by the client, or by the means by which the Consultation, Claim and Clarification was presented, indicating the reasons that support it and, if applicable, attaching the respective documentation.

In case of any Inquiry, Complaint or Clarification, please send it to:

Anabel Castañeda Medrano

Legal Representative | SMBC, S.A.P.I. de C.V., SOFOM, E.N.R.

Torre Virreyes, Pedregal 24, 5th Floor, Col. Molino del Rey, Mexico City, 11040

Tel: +52 (55) 9688 8483 | +52 (55) 2623 1373 | Cel: +52 56 2560 7137

E-mail: anabel.castaneda@smbcsofom.com

If you are not satisfied with the measures adopted by SMBC SOFOM to resolve your Consultation, Complaint or Clarification, we suggest you contact the National Commission for the Protection and Defense of Users of Financial Services, a public agency whose purpose is to protect and defend the rights and interests of the public user of financial services provided by public, private and social sector institutions duly authorized to operate in Mexico.

CONDUSEF also has User Service Units, through which Users may submit written documents establishing their disagreement with any Financial Institution under the supervision of said authority.

Bureau of Financial Entities

It is a consultation and dissemination tool with which you can learn about the products offered by financial institutions, their commissions and fees, user complaints, unhealthy practices, administrative sanctions imposed on them, abusive clauses in their contracts and other relevant information to inform you about their performance.

With the Financial Entities Bureau, you will be able to know who is who in banks, insurance companies, multiple purpose financial companies, savings banks, AFORES, among other entities.

With this, you will be able to compare and evaluate the financial institutions, their products and services and you will have more elements to choose what is most convenient for you.

This information will be useful for you to choose a financial product and also to know and use better the ones you already have.

This Bureau of Financial Institutions is a tool that can contribute to the country's economic growth by promoting competition among financial institutions; that will promote transparency by disclosing information to users on their performance and the products they offer; and that will facilitate responsible management of financial products and services by providing detailed information on their characteristics.

This may result in greater social welfare, because by bringing together in a single space such diverse information from the financial system, the user will have more elements to optimize his/her budget, to improve his/her personal finances, to correctly use the credits that will strengthen his/her economy and to obtain the insurance that will protect it, among other aspects.

The information corresponds solely to SMBC, S.A.P.I. de C.V., SOFOM, E.N.R., to obtain information on the entire sector to which it corresponds, you can access the site http://www.buro.gob.mx

Data privacy notice

I. DATA CONTROLLER

SMBC, S.A.P.I. de C.V., SOFOM, E.N.R. (hereinafter, “SMBC SOFOM”) with legal domicile in Torre Virreyes - Pedregal No. 24, Piso 5, Int.502-A, Col. Molino del Rey, Delegación Miguel Hidalgo, Ciudad de México, C.P. 11040, when collecting your personal data, is responsible for its use and protection.

II. PERSONAL DATA

SMBC SOFOM shall collect from you (hereinafter the “Data Subject”) the following personal data as shareholder of one of our clients:

- Contact Data;

- Identification Data;

- Location Data;

- Employment Data; and

- Economic Data, as applicable.

III. SENSITIVE PERSONAL DATA

SMBC SOFOM doesn’t collect any sort of sensitive data from the Data Subject. By sensitive personal data we may understand any personal data that intrudes the most intimate circle of the Data Subject or that if used inappropriately, it could lead to discrimination or severe risk for the Data Subject in accordance to the Mexican Data Privacy Law (the “Law”). It is considered particularly sensible all data that could reveal racial or ethnic origin, present or future health conditions, genetic information, religious, philosophical, or moral beliefs, trade union membership, political opinions or sexual preference.

IV. COLLECTING MEANS AND UPDATE

The personal data will be collected while always observing the fulfilment of principles such as lawfulness, consent, information, quality, finality, proportionality, and responsibility. Personal data will be collected in proper and updated databases by:

- Local means,

- Remote or electronic,

- Optical, or

- Other technologies which allow to gather the data automatically or at the same time the Data Subject contacts SMBC SOFOM.

V. PROCESSING PURPOSES

The processing of personal data will constringe exclusively to the fulfilment of the purposes foreseen in this section. Therefore, the processing of personal data will exclusively be the one that results necessary, adequate and relevant in terms with the purposes listed in this section.

- The primary purposes, which originate and are necessary, to maintain and comply the legal relationship between SMBC SOFOM and the Data Subject, are the following:

- Identify the Data Subject and integrate his file.

- Incorporate data on legal instruments to formalize the agreements, in which the client you represent or from whom you are shareholder, pretends to contract with SMBC SOFOM, if applicable;

- Assign or transfer to a third party, by any means, rights and/or obligations derived from said contracts, provided that it is in the interest of the Data Subject;

- Use the personal data, in any action or procedure for judicial or extrajudicial recovery; and

- Comply with all applicable laws, regulations and general dispositions.

- The secondary purposes that aren’t necessary for the maintenance and fulfilment of the legal relationship between SMBC SOFOM and the Data Subject, are the following:

- Delivery of news, invitations to SMBC SOFOM and SUMITOMO MITSUI BANKING CORPORATION’s events and/or its’ subsidiaries.

- Surveys for improving our services.

- Publicity, marketing and/or product advertising, and/or services offered by SMBC SOFOM to the Data Subject, by any material or electronic mean.

VI. DATA TRANSFERS

The personal data of the Data Subject shall be transferred in a national and international level, to individuals or entities located within the following types, categories or sectors, who will assume the same obligations that SMBC SOFOM has. Said data transfer will be done exclusively with the following purposes:

A. To SUMITOMO MITSUI BANKING CORPORATION, to other parent companies, subsidiaries or affiliates under the control of SMBC SOFOM, or to other holding companies or any corporation belonging to the SMBC SOFOM group that operates under the same internal procedures and policies, with the purpose of:

- Identify the Data Subject and integrate his file.

- Incorporate data on legal instruments to formalize the agreements, in which the client you represent or from whom you are shareholder, pretends to contract with SMBC SOFOM, if applicable;

- Assign or transfer to a third party, by any means, rights and/or obligations derived from said contracts, provided that it is in the interest of the Data Subject;

- Use the personal data, in any action or procedure for judicial or extrajudicial recovery;

- Comply with all applicable laws, regulations and general dispositions;

- Share it with national and international authorities to fulfil any law, regulation or legal disposition, if appliable; and

- Any other permitted transfer pursuant to Law.

Please consider that your consent shall not be needed to carry out:

- the transfer described in the aforementioned section A., because is the hypothesis provided by the section III of article 36 of the Federal Law on Protection of Personal Data Held by Private Parties and

- those transferences within the hypothesis provided by the article 36 of the Federal Law on Protection of Personal Data Held by Private Parties.

VII. ARCO RIGHTS

If at any moment the Data Subject by himself or through a legal representative duly authorized, wishes to exercise his rights to access, rectification, cancelation or opposition to process his personal data (the “ARCO Rights”), he might request a format to exercise such rights by any of the following means:

- Asist personally to the “Personal Data Protection Department” domiciled in Torre Virreyes - Pedregal No. 24, Piso 5, Int.502-A, Col. Molino del Rey, Delegación Miguel Hidalgo, Ciudad de México, C.P. 11040, Tel: +52 (55) 9688 8483 | +52 (55) 2623 1373 | Cel: +52 56 2560 7137 within the following operating hours: Monday to Friday from 9:00 to 14:00 and 16:00 to 19:00 hours; or

- Via e-mail to anabel.castaneda@smbcsofom.com, addressed to the “Personal Data Protection Department”, with the name and contact data of the Data Subject.

The format to exercise of ARCO Rights shall be filled out, signed and filed along with the following documents in order to authenticate the Data Subject:

- Official and valid ID of the Data Subject (INE credential, Passport, Military Service Document or Professional Certificate).

- In case of exercising the ARCO Rights is done through the legal representative of the Data Subject, you shall provide the official ID of the representative along with the notarized power of attorney which acknowledges the legal of the Data Subject.

- A proof of residency or any other means to communicate the response to the Data Subject’s request.

- The clear and previse description of the personal data according to the ARCO Right wished to claim. It is especially important when exercising the rectification, to include documentation which proofs the modification requested according to the personal data that wants to be rectified.

SMBC SOFOM shall reply to such form 20 (twenty) business days following the date in which the form was received. The resolution adopted by SMBC SOFOM shall be notified to the Data Subject by means elected by the Data Subject in the form for the exercise of ARCO Rights. In case the resolution adopted is proceeding, SMBC SOFOM will make it effective in the following 15 (fifteen) days to the date in which the resolution is notified. It’s important to mention that these time frames may be extended only once and in the same time period when and if the circumstances justify it, with previous notification of the Data Subject.

In the case You wish to revoke your consent or refuse to the process of your personal data for the secondary purposes, after this privacy notice is signed, You shall go to the Personal Data Protection Department or send an e-mail to the aforementioned address. Regarding personal data not collected directly from the Data Subject, he shall have 5 (five) business days to refuse to the process of his personal data.

VIII. MEANS TO LIMIT THE USE AND DISCLOSURE OF PERSONAL DATA

SMBC SOFOM has created an exclusion list for individuals that do not wish to receive advertisement or information from SMBC SOFOM, by means of which You could limit the use of your personal data. If You receive advertisement or information from SMBC SOFOM and You don’t want to keep receiving it, You shall send an e-mail with your full name to anabel.castaneda@smbcsofom.com, requesting your elimination from said list. Through that same e-mail You might ask for more information regarding said list.

Additionally, the Data Subject can register in the Public Registry of Users provided by the Federal Law on Protection and Defense of the User of Financial Services with the purpose of limiting the use and disclosure of his personal data. This Registry (REUS), allows to the Data Subject to register in a database to limit promotional calls or e-mails, seeking to maintain the safety of his privacy and avoid the troubles caused by said calls or e-mails. The Data Subject shall be able to register to the REUS through the process established in the following website: www.condusef.gob.mx

IX. CHANGES TO THE PRIVACY NOTICE

This privacy notice will be made available to the Data Subject through printed, digital and visual formats, and will be available at SMBC SOFOM’s web page. Likewise, the amendments made to this privacy notice will be sent to the Data Subject by said means.

It is hereby noted that this privacy notice is made in Spanish and English, on the understanding that, in the event of any controversy arising from their interpretation, the Spanish version shall prevail.

By singing this privacy notice, the Data Subject consents that his personal data shall be processed by SMBC SOFOM, as provided by privacy notice, intended for the purposes aforementioned and transferred only to the third parties provided herein.

Spanish Version

Acerca de nosotros

Las Sociedades Financieras de Objeto Múltiple (SOFOMes) son un tipo de sociedades en México, cuyo objeto principal es la realización de una o más de las actividades de otorgamiento de crédito, arrendamiento o factoraje financieros; este tipo de sociedades deben contar con un registro vigente ante la Comisión Nacional para la Protección y Defensa de los Usuarios de Servicios Financieros.

Este tipo de sociedades funcionan de manera similar a un banco, excepto que no se les permite la captación de recursos del público en general y no están fuertemente supervisadas por las autoridades mexicanas.

En marzo de 2015, SMBC SOFOM inició oficialmente sus operaciones con un solo producto autorizado - Préstamos a Plazo (Single Draw).

Productos y servicios

Actualmente SMBC SOFOM cuenta con los siguientes servicios:

- Préstamos a plazo únicos y de disposición diferida (sujetos a la cobertura de liquidez mediante capital)

- Crédito Revolvente / GTFD (sujeto a la cobertura de liquidez utilizando el capital)

- Financiamiento de Proyectos - Utilizando la facilidad de financiamiento de Banobras (Banco de Desarrollo) (financiamiento a largo plazo en MXN)

- Arrendamientos financieros (MXN o USD)

- Derivados

Unidad Especializada de Atención a Usuarios

La Unidad Especializada de Atención a Usuarios (UNE) de SMBC SOFOM tiene por obje

o atender las Consultas, Reclamaciones y Aclaraciones de los Usuarios de los servicios prestados por ésta y deberá proporcionar a la Comisión Nacional para la Protección y Defensa de los Usuarios de Servicios Financieros (CONDUSEF) la información relativa a la UNE y la manera de identificar o localizar a su titular.

En ese sentido, SMBC SOFOM deberá recibir las referidas Consultas, Reclamaciones y Aclaraciones por parte de sus clientes, a través de los Medios de Recepción que designe para tales efectos, acusar de recibo a los clientes, asignar número de folio e indicar el tiempo de respuesta o resolución. Asimismo, deberá comunicar al cliente la resolución o respuesta correspondiente por el medio que éste haya indicado, o bien, por el que se presentó la Consulta, Reclamación y Aclaración, indicando los motivos que la sustenten y, en su caso, adjuntando la documentación respectiva.

En caso de cualquier Consulta, Reclamación o Aclaración, favor de enviarla a:

Anabel Castañeda Medrano

Representante Legal | SMBC, S.A.P.I. de C.V., SOFOM, E.N.R.

Torre Virreyes, Pedregal 24, Piso 5, Col. Molino del Rey, Cd. de México, 11040

Tel: +52 (55) 9688 8483 | +52 (55) 2623 1373 | Cel: +52 56 2560 7137

E-mail: anabel.castaneda@smbcsofom.com

Si no está satisfecho con las medidas adoptadas por SMBC SOFOM para resolver su Consulta, Reclamación o Aclaración, le sugerimos contactar la Comisión Nacional para la Protección y Defensa de los Usuarios de Servicios Financieros, organismo público, el cual tiene por objeto la protección y defensa de los derechos e intereses del público usuario de los servicios financieros, que prestan las instituciones públicas, privadas y del sector social debidamente autorizadas para operar en México.

La CONDUSEF también cuenta con Unidades de Atención a Usuarios, mediante los cuales se pueden presentar escritos que establezcan la inconformidad del Usuario con alguna Entidad Financiera que se encuentre bajo la supervisión de dicha autoridad.

Buró de Entidades Financieras

Es una herramienta de consulta y difusión con la que podrás conocer los productos que ofrecen las entidades financieras, sus comisiones y tasas, las reclamaciones de los usuarios, las prácticas no sanas en que incurren, las sanciones administrativas que les han impuesto, las cláusulas abusivas de sus contratos y otra información que resulte relevante para informarte sobre su desempeño.

Con el Buró de Entidades Financieras, se logrará saber quién es quién en bancos, seguros, sociedades financieras de objeto múltiple, cajas de ahorro, afores, entre otras entidades.

Con ello, podrás comparar y evaluar a las entidades financieras, sus productos y servicios y tendrás mayores elementos para elegir lo que más te convenga.

Esta información te será útil para elegir un producto financiero y también para conocer y usar mejor los que ya tienes.

Este Buró de Entidades Financieras, es una herramienta que puede contribuir al crecimiento económico del país, al promover la competencia entre las instituciones financieras; que impulsará la transparencia al revelar información a los usuarios sobre el desempeño de éstas y los productos que ofrecen y que va a facilitar un manejo responsable de los productos y servicios financieros al conocer a detalle sus características.

Lo anterior, podrá derivar en un mayor bienestar social, porque al conjuntar en un solo espacio tan diversa información del sistema financiero, el usuario tendrá más elementos para optimizar su presupuesto, para mejorar sus finanzas personales, para utilizar correctamente los créditos que fortalecerán su economía y obtener los seguros que la protejan, entre otros aspectos.

La información corresponde únicamente a SMBC, S.A.P.I. de C.V., SOFOM, E.N.R., para conocer la información de todo el sector al que corresponda, se podrá acceder al sitio http://www.buro.gob.mx

Aviso de privacidad para representantes legales y/o accionistas de clientes

I. RESPONSABLE

SMBC, S.A.P.I. de C.V., SOFOM, E.N.R. (en lo sucesivo, “SMBC SOFOM”) con domicilio en Torre Virreyes - Pedregal No. 24, Piso 5, Int.502-A, Col. Molino del Rey, Delegación Miguel Hidalgo, Ciudad de México, C.P. 11040 al momento de recabar sus datos personales, es responsable del uso y protección de los mismos.

II. DATOS PERSONALES

SMBC SOFOM recabará de usted (en adelante el "Titular") los siguientes datos personales en su calidad de accionista de uno de nuestros clientes:

- Datos de Contacto;

- Datos de Identificación;

- Datos de Localización;

- Datos Laborales; y

- Datos Patrimoniales, según aplique.

III. DATOS PERSONALES SENSIBLES

SMBC SOFOM no recaba ningún tipo de datos personales sensibles del Titular. Por datos personales sensibles debemos entender de conformidad con la Ley Federal de Protección de Datos Personales en Posesión de los Particulares (la “Ley”), aquellos datos personales que afecten la esfera más íntima de su Titular, o cuya utilización indebida pueda dar origen a discriminación o conlleve un riesgo grave para éste. En particular, se consideran sensibles aquellos que puedan revelar aspectos como origen racial o étnico, estado de salud presente y futuro, información genética, creencias religiosas, filosóficas y morales, afiliación sindical, opiniones políticas o preferencia sexual.

IV. MEDIOS DE OBTENCIÓN Y ACTUALIZACIÓN

Los datos personales serán obtenidos observando siempre el cumplimiento de los principios de licitud, consentimiento, información, calidad, finalidad, lealtad, proporcionalidad y responsabilidad. Dichos datos serán contenidos en bases de datos pertinentes y actualizadas a través de:

- Medios locales

- Remotos o electrónicos,

- Ópticos, o

- Mediante el uso de otras tecnologías que permitan recabar los datos de forma automática o simultánea al momento en que el Titular contacte a SMBC SOFOM.

V. FINALIDADES DEL TRATAMIENTO

El tratamiento de datos personales únicamente se limitará al cumplimiento de las finalidades previstas en este apartado. Por esto mismo, el tratamiento de datos personales será exclusivamente el que resulte necesario, adecuado y relevante en relación con las finalidades previstas en este apartado.

- Las finalidades primarias que dan origen y son necesarias para el mantenimiento y cumplimiento de la relación jurídica entre SMBC SOFOM y el Titular son las siguientes:

- Llevar a cabo la identificación y conocimiento del Titular, así como la integración de su expediente;

- En su caso, incorporar sus datos en los instrumentos jurídicos necesarios para la formalización de los contratos que el cliente del cual Usted es accionista o representante pretende celebrar con SMBC SOFOM;

- Ceder o transmitir a un tercero, mediante cualquier medio, los derechos y/u obligaciones derivadas de los contratos antes señalados, siempre y cuando dicho contrato sea en interés del Titular;

- Utilizar los datos personales, en cualquier tipo de acto o diligencia de cobranza judicial o extrajudicial; y

- Cumplir con todas las leyes, reglamentos y disposiciones de carácter general aplicables.

- Las finalidades secundarias que no son necesarias para el mantenimiento y cumplimiento de la relación jurídica entre SMBC SOFOM y el Titular, son las siguientes:

- Envío de noticias, invitaciones a eventos de SMBC SOFOM y de SUMITOMO MITSUI BANKING CORPORATION y/o sus subsidiarias y filiales.

- Encuestas para mejorar nuestro servicio.

- La mercadotecnia, publicidad y/o promoción de los productos y/o servicios que sean ofrecidos por SMBC SOFOM al Titular, por cualquier medio material y/o electrónico.

VI. TRANSFERENCIA DE DATOS

Los datos personales del Titular se transferirán a nivel nacional e internacional, a las personas o entidades ubicadas en los siguientes tipos, categorías o sectores, quienes asumirán las mismas obligaciones que le corresponden a SMBC SOFOM. Dicha transferencia de datos se hará exclusivamente con las siguientes finalidades:

A. SUMITOMO MITSUI BANKING CORPORATION, a otras sociedades controladoras, subsidiarias o afiliadas bajo el control común de SMBC SOFOM, o a una sociedad matriz o a cualquier sociedad del mismo grupo de SMBC SOFOM, que operen bajo los mismos procesos y políticas internas, con la finalidad de:

- Llevar a cabo la identificación y conocimiento del Titular, así como la integración de su expediente;

- En su caso, incorporar sus datos en los instrumentos jurídicos necesarios para la formalización de los contratos que el cliente del cual Usted es accionista o representante, pretende celebrar con SMBC SOFOM;

- Ceder o transmitir a un tercero, mediante cualquier medio, los derechos y/u obligaciones derivadas de los contratos antes señalados, siempre y cuando dicho contrato sea en interés del Titular;

- Utilizar los datos personales, en cualquier tipo de acto o diligencia de cobranza judicial o extrajudicial;

- Cumplir con todas las leyes, reglamentos y disposiciones de carácter general aplicables;

- Compartirlo a las autoridades nacionales y extranjeras competentes, con la finalidad de dar cumplimiento a alguna ley, reglamento o disposición legal aplicable; and

- Cualquier otra transferencia permitida conforme a la Ley.

Por favor considerar que no será necesario tener su consentimiento para llevar a cabo:

- la transferencia indicada en el inciso A. de la sección anterior, por encontrarse en el supuesto establecido en la fracción III del artículo 36 de la Ley Federal de Protección de Datos Personales en Posesión de los Particulares y

- aquellas transferencias que se encuentren dentro de los supuestos establecidos en el Artículo 36 de la Ley Federal de Protección de Datos Personales en Posesión de los Particulares.

VII. DERECHOS “ARCO”

Si en cualquier momento el Titular por sí o mediante su representante legal debidamente autorizado, desea ejercer sus derechos de acceso, rectificación, cancelación u oposición al tratamiento de sus datos personales (los “Derechos ARCO”) podrá solicitar un formato para ejercer dichos derechos, a través de cualquiera de los siguientes medios:

- Asistir personalmente al “Departamento de Protección de Datos Personales” con domicilio en Torre Virreyes - Pedregal No. 24, Piso 5, Int.502-A, Col. Molino del Rey, Delegación Miguel Hidalgo, Ciudad de México, C.P. 11040 Tel: +52 (55) 9688 8483 | +52 (55) 2623 1373 | Cel: +52 56 2560 7137 y, en un horario de atención de lunes a viernes de 9:00 a 14:00 horas y de 16:00 a 19:00 horas; o

- Mediante el envío de un correo electrónico a la dirección anabel.castaneda@smbcsofom.com, a la atención de Departamento de “Protección de Datos Personales” con el nombre y los datos de contacto del Titular.

El formato de ejercicio de Derechos ARCO se deberá llenar, firmar y presentarse acompañado de la siguiente documentación, a fin de que pueda llevarse a cabo la autenticación del Titular:

- Identificación oficial vigente del Titular (Credencial del Instituto Nacional Electoral, Pasaporte, Cartilla del servicio Militar Nacional o Cédula Profesional).

- En los casos en que el ejercicio de los Derechos ARCO se realice a través del representante legal del Titular, deberá acompañarse la identificación oficial del representante, así como el poder correspondiente protocolizado que acredite la representación legal conferida por el Titular.

- Un comprobante de domicilio o cualquier otro medio para comunicarle la respuesta de su solicitud al Titular.

- La descripción clara y precisa de los datos personales respecto del derecho que se pretende ejercer. Es especialmente importante que cuando se ejerza el derecho de rectificación, se exhiba la documentación que acredite el cambio solicitado de acuerdo con los datos personales a rectificar.

SMBC SOFOM responderá a dicho formato después de 20 (veinte) días hábiles contados a partir de la fecha en que fue recibida dicha solicitud. La resolución adoptada por SMBC SOFOM será comunicada al Titular a través de las opciones elegidas por éste en el formato de ejercicio de Derechos ARCO. Asimismo, en caso de que dicha resolución sea procedente, SMBC SOFOM la hará efectiva en un plazo de 15 (quince) días siguientes a la fecha en que se comunica la respuesta. Es menester mencionar que dichos plazos podrán ser ampliados en una única ocasión y sólo por un periodo igual, siempre y cuando así lo justifiquen las circunstancias del caso, previa notificación al Titular.

En caso de que Usted desee revocar su consentimiento o negarse al tratamiento de sus datos personales para las finalidades secundarias, con posterioridad a la firma del presente aviso de privacidad, deberá acudir al Departamento de Protección de Datos Personales o enviar un correo electrónico a la dirección indicada en la sección anterior. Tratándose de datos personales que no se hubieren recabado directamente del Titular, éste tendrá 5 (cinco) días hábiles para manifestar su negativa al tratamiento de sus datos personales.

VIII. MEDIOS PARA LIMITAR EL USO Y DIVULGACIÓN DE LOS DATOS PERSONALES

SMBC SOFOM ha creado un listado de exclusión para personas que no deseen recibir publicidad o información de SMBC SOFOM mediante el cual Usted podrá limitar el uso de sus datos personales. Si Usted recibe publicidad o información de SMBC SOFOM y no desea seguir recibiéndola, podrá enviar un correo electrónico con su nombre completo a anabel.castaneda@smbcsofom.com, solicitando su eliminación de la lista de distribución con base en la cual se lleva a cabo el envío de la información o publicidad. En el mismo correo electrónico podrá solicitar más datos acerca de este listado.

Adicionalmente, el Titular podrá inscribirse en el Registro Público de Usuarios conforme a la Ley de Protección y Defensa al Usuario de Servicios Financieros con la finalidad de limitar el uso y divulgación de sus datos personales. Este registro (REUS), permite que el Titular se inscriba en una base de datos a fin de restringir llamadas promocionales o correos electrónicos, buscando mantener a salvo su privacidad y evitar las molestias que causan estas llamadas o envío de información. El Titular podrá registrarse al REUS a través de los medios que se establecen en la siguiente página de Internet: www.condusef.gob.mx.

IX. CAMBIOS AL AVISO DE PRIVACIDAD

El presente aviso de privacidad se pondrá a disposición del Titular a través de formatos impresos, digitales. y visuales, y estará disponible para su consulta en la página de internet de SMBC SOFOM. De igual forma, las modificaciones que se hagan al presente aviso de privacidad, serán enviadas al Titular por dichos medios.

Se toma nota de que el presente aviso de privacidad se transcribe en idioma inglés y español, en el entendido de que, en caso de cualquier controversia sobre su interpretación, la versión en español prevalecerá.

Al firmar el presente aviso de privacidad, el Titular consiente que sus datos personales sean tratados por SMBC SOFOM conformidad con lo previsto en el presente aviso de privacidad, destinados para las finalidades indicadas en el presente y transferidos a los terceros establecidos aquí establecidos

Contacto

Anabel Castañeda Medrano

Representante Legal | SMBC, S.A.P.I. de C.V., SOFOM, E.N.R.

Torre Virreyes, Pedregal 24, Piso 5, Col. Molino del Rey, Cd. de México, 11040

Tel: +52 (55) 9688 8483 | +52 (55) 2623 1373 | Cel: +52 56 2560 7137

Email: anabel.castaneda@smbcsofom.com